Everything you’ve always wanted to know about staying financially savvy while living abroad!

So I was all ready to write a post this week on deciding a time frame for moving abroad, when a miraculous thing happened. I was finally approved for income based repayment on my student loans, and my official payment is $0 a month! Which I was pretty much banking on in order to keep this whole living in Thailand and not earning much in terms of dollars thing working. What I realized as I was going through this process is that people often aren’t aware of all of their options when it comes to managing debt (student debt in particular, which exists in it’s own wacky world of rules and regulations).

I’ll preface this entire post with the fact that I am a pretty thrifty person, and I’ve always been conscious of how I spend my money. Until recently, I had a pretty good nest egg built up that has sustained me through employment dry spells and unexpected expenses; even though months of underemployment and two long distance moves took their toll, I’m confident that I’ll be able to get back to where I was in a respectable amount of time.

Because it’s a huge factor for recent grads (like me!) looking into managing a move abroad, I want to start by talking about staying on top of student debt when your salary, once converted to dollars, is pathetically small. Many people that I’ve talked to don’t realize that you can qualify for a $0 per month payment, think their only option is deferment or forbearance, or are too afraid of the paperwork to bother. IBR has a significant advantage over deferment or forbearance in that it counts as payments made towards the golden 20/25 year forgiveness date (or 10 years if you work in public service). Even if your payments are nothing, it still counts. Meaning you’ll spend less time in debt and pay less in interest over the life of the loan. Yay!

Once you have moved and found employment abroad, qualifying for IBR is fairly straightforward and easy; you submit your most recent tax documents online, and then submit proof of your current income directly to whatever company services your loan. For me, this meant a copy of my teaching contract, which includes my pay rate, and a conversion of this rate from baht to US dollars (I submitted a screen shot of an online conversion tool). I make 31,100 baht per month, which comes out to $1,045; if I were living in the US, I’d be far below the poverty line. In Thailand, I live in a nice apartment in a good neighborhood, eat all of my meals out, travel several times a year, and split some of my earnings between both savings and student loan payments.

Even if your payment is $0 a month, it’s crucial to stay on top of the interest accruing on your loans. This amount gets turned into principal at the end of each year, meaning if you don’t pay it off you’ll be paying interest on your interest! At a minimum, you don’t want your debt to go up while you’re abroad, so making payments to cover your interest is really, really important.

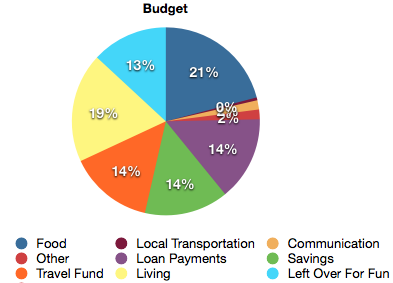

Keeping in mind that I want to make payments on my loan interest, build up my savings and travel fund, and live comfortably, I’ve set myself this budget for the year:

The numbers (in baht) break down like this:

- Living (rent, utilities, gym) – 5,860

- Food (including booze and occasional groceries) – 6,500

- Transportation (scooter gas mostly, and occasional song taew rides or bike maintenance) – 150

- Communication (cell phone and internet) – 500

- Loan Payment – 4,500

- Savings – 4,500

- Travel Fund – 4,500

- Other (medications, laundry, school supplies) – 520

- Left over for fun – 4,075

Even after all of my expenses are paid and almost half of my salary is set aside for savings, travel and loan payments, I still have a little over 4,000 baht each month for whatever else I want (massages, trips to the movies, shopping, really nice dinners, etc). Even though it’s only about $130, it’s actually quite a lot of money here and after months on a tight budget it’ll be weird to get used to having cash to burn!

Although it may seem daunting to keep up with debt on such a tiny salary, it’s possible if you stay smart, know your options, and work with what you’ve got!